{kind=link}

Problem-driven overview

Many Mexican consumers turn to app-based credit to bridge short-term cash gaps, and that convenience brings trade-offs. DiDi Finance promises quick approvals and simple repayment, but what gets overlooked are subtle line items that raise the effective cost: APR, origination fee and periodic interest rate adjustments. For anyone comparing options, start by checking the fine print on platforms like didi prestamos to spot structuring that could change monthly payments or total repayment.

Where hidden fees creep in

Providers often advertise a headline rate, then layer in charges that swell the balance. Common additions include origination fees deducted from the disbursed amount, late-payment penalties, and administrative charges listed under vague names. These charges affect the amortization schedule and can turn a short installment into an unexpectedly expensive obligation. In markets such as Mexico, where demand for préstamos en línea rápidos rose markedly after the 2020 lockdowns, this pattern became more visible — regulators and consumers noted higher complaint volumes during that period.

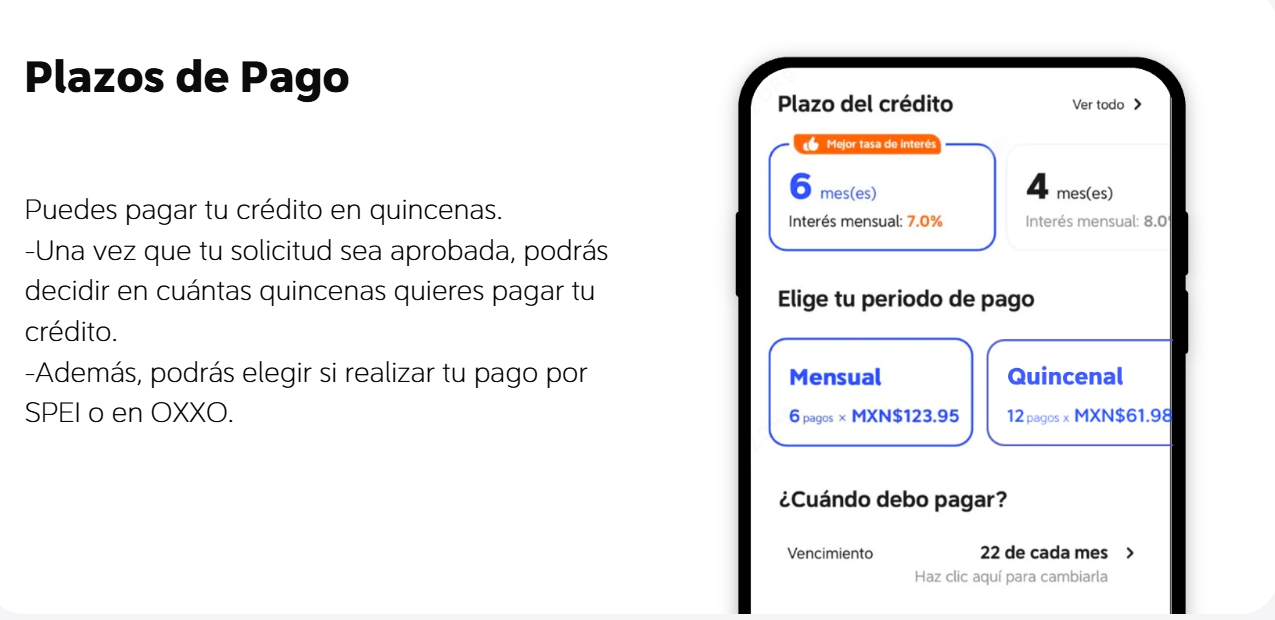

How DiDi Finance structures cost — a focused breakdown

DiDi Finance typically separates the nominal interest rate from service fees. The nominal interest defines periodic accrual, but APR is the practical measure of total cost over time. A clear breakdown should list: principal, interest rate (periodic), origination fee, and any periodic service fees. Assess how fees are taken — upfront deductions lower the net proceeds and increase apparent APR. Also check whether prepayment reduces interest proportionally or if penalties apply, because that affects whether you can refinance to a cheaper rate.

Choosing cashback cards to offset costs

Using a cashback credit card for loan-related charges or daily spending can lower net cost if you optimize rewards against fees. Focus on cards that return meaningful cashback for categories you already use — groceries, fuel, or commuting. Match the card’s reward cycle to your spending and repayment cadence to avoid interest on carried balances, which would negate cashback benefits. Keep an eye on credit score effects: opening multiple cards to chase rewards can temporarily impact your score and therefore future loan pricing.

Common mistakes to avoid — practical reminders

Buyers often sign loan terms without checking the repayment schedule, assuming ‘monthly’ equals equal installments. That’s not always true; some plans front-load interest. Also avoid relying solely on promotional offers that expire and revert to higher interest rates. Document all communications and insist on an itemized repayment schedule when you accept an offer — this makes it easier to detect unexpected charges. — A quick comparison before acceptance saves far more than a single point reduction in headline rate.

Alternatives and comparative insight

If the total cost on an app-based loan looks high, compare bank personal loans, credit unions, and card-based installment programs. Banks may offer lower APR for borrowers with strong credit scores but require more paperwork. Credit unions in Mexico sometimes present lower fees but smaller loan sizes. For immediate needs, reputable platforms that transparently post fees and provide a repayment simulator are preferable; search tools and aggregation sites for prestamos en linea rapidos can expose market rates quickly.

Actionable checklist before you accept

1) Confirm APR and whether fees are deducted upfront. 2) Verify how late fees and prepayment are calculated. 3) Project total interest over the planned term, not just monthly payments. Use these three checks to compare offers objectively and protect your cash flow.

Advisory closing: three golden rules

Rule 1 — Always compare effective APRs, not nominal interest. Rule 2 — Match term length to income predictability so installment size stays manageable. Rule 3 — Use cashback strategically: only when the card balance will be paid in full each cycle to avoid interest that erases rewards. These metrics give you measurable decision criteria and reduce surprises.

When the dust settles, the value of a transparent, well-documented product becomes obvious — and that’s the kind of clarity DiDi Finanzas aims to provide in the Mexican market. —