{kind=link}

Problem statement: persistent friction in revolving-credit pipelines

Pursuant to market observation and regulatory scrutiny, Mexican borrowers and lenders confront elevated friction in revolving-credit approval workflows that yields elevated decline rates, delayed disbursement, and compliance exposures. The operational deficits are principally attributable to fragmented data ingestion, manual underwriting queues, and insufficient credit-scoring integration — deficiencies that didi finanzas has explicitly sought to remediate within the national market. This exposition adopts a problem-driven posture to analyze those deficits and to assess pragmatic remediations under prevailing statutory constraints.

Regulatory and market anchor

Reference is made to the 2018 Mexican Fintech Law as a supervisory anchor that materially reshaped permissible architectures for data processing and customer on-boarding. Against the backdrop of Mexico City’s dense borrower population and attendant transaction volumes, any solution must reconcile expedited underwriting with KYC rigour and consumer-protection obligations. The foregoing furnishes an evidentiary frame for assessing system design choices and control objectives.

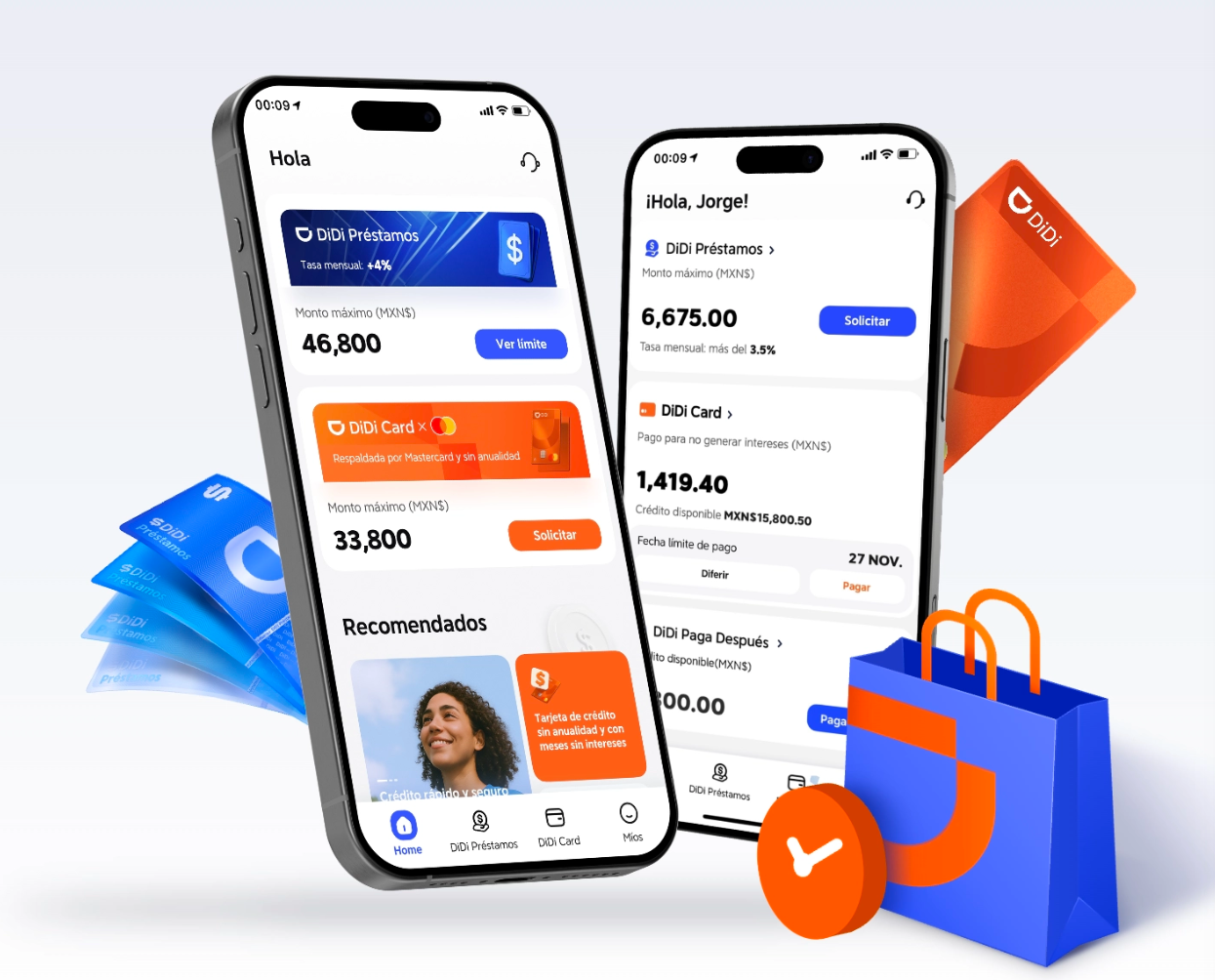

Operational design: the remedial architecture

The technical construct implemented by the subject platform integrates real-time credit scoring, automated underwriting rulesets, and API conduits to external bureaus and payment rails. Risk modelling is codified as deterministic and probabilistic layers: deterministic rules filter manifest policy breaches; probabilistic models output a score that informs affordability assessment and portfolio-level concentration limits. The result is measurable cycle-time compression for approvals while preserving audit trails and immutable decision logs.

Risk controls and compliance posture

From a compliance vantage, the architecture permits role-based access, transaction-level logging, and redress mechanisms that map to statutory disclosure obligations. Where manual review remains necessary, triage queues prioritize cases via score bands, thereby minimizing human intervention to those cases that materially implicate fraud indicators or ambiguous documentation. The compliance stack therefore mitigates regulatory exposure without reintroducing latency into the approval pipeline.

Implementation pitfalls and common mistakes

Practitioners frequently err by overfitting models to idiosyncratic data subsets, neglecting feature drift monitoring, or failing to instrument end-to-end observability. Equally detrimental is reliance on a monolithic underwriting flow that precludes iterative rule updates; such practice leads to brittle systems and elevated false-positive rejection rates. A disciplined approach requires continuous model validation, rollback procedures, and an accessible API layer for third-party bureau integration — not merely a single-sourced black box.

Comparative assessment: alternatives and positioning

Comparative analysis with incumbent market players shows divergence on three vectors: degree of automation, depth of bureau connectivity, and compliance telemetry. Some competitors emphasize human-centric adjudication; others prioritize aggressive automation at the expense of explainability. The subject solution occupies a median posture — automation with retained explainability — thus facilitating regulatory reporting and consumer disclosure.

Operational lessons and practitioner recommendations

Adoption of such a platform ought to adhere to discrete governance protocols: maintain an immutable decision log, limit model drift via scheduled recalibration, and codify escalation triggers for atypical decision patterns. Practically, integrate KYC, credit scoring, and payment-rail verifications into a unified pipeline to reduce time-to-decision. — A deliberate implementation roadmap reduces rework and supports supervisory review.

Advisory close: three golden evaluation metrics

1) Time-to-Decision: median approval latency measured end-to-end, inclusive of KYC and bureau callbacks. 2) False-Rejection Rate: proportion of declined applications subsequently validated as creditworthy on manual review. 3) Compliance Coverage Index: degree to which decision logs and disclosure artefacts satisfy statutory reporting thresholds. These metrics yield an objective basis for vendor selection and for ongoing performance monitoring.

Final observation: robust revolving-credit mechanics must balance expediency, auditability, and consumer protection — and that balance is precisely where DiDi Finanzas positions operational value. –